The Ultimate 50/30/20 Budget Rule Guide for Asian Professionals

Are you an Asian professional struggling to manage your finances effectively? The 50/30/20 budget rule offers a simple yet powerful framework to gain control over your money. This popular method helps you balance needs, wants, and savings without complex spreadsheets. It’s about creating a sustainable financial lifestyle that aligns with your goals. In this comprehensive guide, Financial Forms For Asia will break down the 50/30/20 budget rule and show you how to adapt it to the unique financial landscape of modern Asia.

What Is the 50/30/20 Budget Rule and Why Is It So Popular?

Before diving into how to apply this method, it’s essential to understand its core principles. The beauty of the 50/30/20 budget rule lies in its simplicity and flexibility, making it an ideal starting point for anyone looking to improve their financial health.

1. The Core Concept Explained

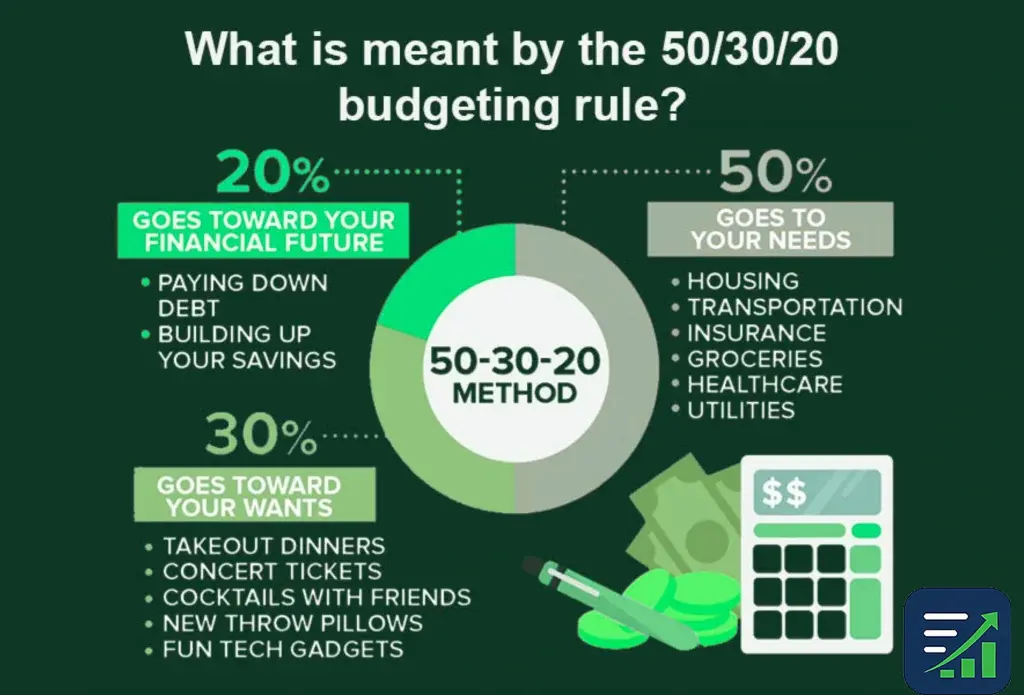

The 50/30/20 budget rule was popularized by U.S. Senator Elizabeth Warren. It suggests dividing your after-tax income into three spending categories.

50% of your income should go towards “Needs”. 30% is allocated for “Wants”. The remaining 20% is for “Savings and Debt Repayment”.

This framework provides a clear guideline. It helps you prioritize spending without tracking every single dollar.

2. The “Needs” Category: 50%

Needs are your essential expenses. These are the bills you must pay to live.

This category includes housing (rent or mortgage), utilities, transportation to work, groceries, and insurance. These are non-negotiable costs.

The goal is to keep these essential expenses at or below half of your take-home pay. This is a key part of the 50/30/20 budget rule.

3. The “Wants” Category: 30%

Wants are non-essential expenses that improve your quality of life. This category is all about lifestyle choices.

It includes things like dining out, shopping for clothes, hobbies, entertainment, and travel. These are things you enjoy but could live without.

Allocating 30% to this category ensures you can enjoy life. It makes the budget feel less restrictive.

4. The “Savings & Debt” Category: 20%

This is arguably the most important category for your future. It focuses on building wealth and financial security.

It includes contributions to your retirement fund, building an emergency fund, investing, and paying off high-interest debt (like credit cards or personal loans).

Consistently saving 20% is a powerful habit. The 50/30/20 budget rule makes this a priority.

5. The Psychological Benefits of Simplicity

One of the biggest reasons for the popularity of the 50/30/20 budget rule is its psychological benefit. Complex budgets with dozens of categories can be overwhelming.

This can lead to “decision fatigue” and cause people to abandon budgeting altogether. The simplicity of three categories reduces this mental burden.

It allows you to focus on the big picture. This makes the 50/30/20 budget rule easier to stick with long-term.

Adapting the 50/30/20 Budget Rule for Asian Professionals

While the 50/30/20 budget rule is a great starting point, it needs adjustments to fit the unique cultural and economic contexts in Asia. Factors like family obligations, high housing costs in major cities, and different savings mentalities play a significant role.

1. Accounting for Family Obligations

In many Asian cultures, supporting parents and extended family is a significant financial responsibility. This often falls under the “Needs” category.

You may need to adjust the 50% allocation for Needs to 55% or even 60%. This means reducing your “Wants” category accordingly.

This cultural nuance is a critical consideration. It makes the standard 50/30/20 budget rule challenging without modification.

2. Navigating High Costs of Living in Major Cities

Professionals in cities like Singapore, Hong Kong, or Tokyo face extremely high housing costs. Rent can easily consume more than 30-40% of after-tax income.

In this case, your “Needs” might again exceed the 50% guideline. It’s important not to feel discouraged by this.

The key is to be flexible. You might need to be more frugal with your “Wants” to maintain your savings goals.

3. Embracing a Higher Savings Rate

Many Asian cultures have a strong tradition of saving. A 20% savings rate might feel too low for some.

If your “Needs” are under control, feel free to increase your savings. You could aim for a 40/30/30 split instead.

This proactive approach to saving aligns well with the principles of the 50/30/20 budget rule while fitting cultural norms.

4. Dealing with Fluctuating Income

Many professionals in Asia, especially freelancers and entrepreneurs, have fluctuating incomes. This can make fixed-percentage budgeting tricky.

A good strategy is to base your 50/30/20 budget rule on your lowest anticipated monthly income. This creates a baseline for your essential needs.

In months where you earn more, allocate the surplus directly to your 20% category. This helps you accelerate your savings and debt repayment goals.

Step-by-Step Guide to Implementing the 50/30/20 Budget Rule

Getting started is the hardest part. This step-by-step guide will walk you through the process of setting up and maintaining your new budget, making the 50/30/20 budget rule a practical tool in your financial toolkit.

1. Calculate Your After-Tax Income

The first step is to know exactly how much money you have to work with. This is your net income, or take-home pay.

Look at your payslip to find the amount after taxes, social security, and other deductions have been taken out.

This number is the foundation of your 50/30/20 budget rule calculations.

2. Track Your Spending for One Month

Before you can categorize, you need to know where your money is going. Track every expense for at least one month.

You can use a notebook, a spreadsheet, or a budgeting app. Be as detailed as possible.

This exercise is often eye-opening. It reveals your true spending habits.

3. Categorize Your Expenses

Now, go through your tracked expenses. Assign each one to one of the three categories: Needs, Wants, or Savings/Debt.

Be honest with yourself. Is your daily gourmet coffee a “Need” or a “Want”?

This step helps you see how your current spending aligns with the 50/30/20 budget rule framework.

4. Analyze and Adjust

Calculate the percentage of your income you’re spending in each category. How does it compare to the 50/30/20 guideline?

If your “Wants” are at 40% and “Savings” are at 10%, you know where you need to make cuts. Look for areas to reduce spending.

The goal is to adjust your habits. To better align with your desired financial goals.

5. Common Pitfalls and How to Avoid Them

A common mistake is miscategorizing expenses. Being too lenient and classifying wants as needs will undermine the budget.

Another pitfall is not reviewing the budget regularly. Your income and expenses can change, so your budget should be a living document.

Finally, don’t be too rigid. The 50/30/20 budget rule is a guideline, not a strict law. Allow for some flexibility to ensure you can stick with it long-term.

Conclusion

The 50/30/20 budget rule provides an excellent, straightforward approach to managing your finances. By categorizing your spending into Needs, Wants, and Savings, you can gain clarity and control over your money without overwhelming yourself. For Asian professionals, adapting this rule to accommodate cultural norms and economic realities is key to its success. We at Financial Forms For Asia believe that with this guide to the 50/30/20 budget rule, you are well-equipped to build a healthier financial future. Start applying the 50/30/20 budget rule today!